Sustainability reporting impacts designers’ work

Good times are ahead for design industries in promoting sustainability solutions, as design and planning have been brought to the center of the EU’s sustainability guidelines. The new policies will also become part of designers work in companies. What exactly is sustainability reporting and how does it affect the activities of designers and companies?

Responsible design is now in demand in almost every sector, both in the design of physical design products and services as well as processes. Designers and companies in the field have a special opportunity to be involved in developing corporate responsibility in the design and usability of products, as well as in the sustainable design of value chains and material flows.

What is the sustainability reporting directive about?

The CSRD (Corporate Sustainability Reporting Directive) obligation first applies to large listed companies, and reporting will start from this year. With the sustainability directive, companies make their sustainability activities of the entire value chain visible. Therefore, it also has an impact on the operations of the companies in the subcontracting chain and could provide a competitive advantage. The sustainability directive applies to the company’s operations within the EU, but the report also records operations outside the EU. Companies from third countries that have significant business operations in the Union must also report on their sustainability.

CSRD Schedule and content:

- 2024 large listed companies (over 500 employees)

- 2025 all companies that fill two of the following criteria: more than 250 employees, turnover over €40 million or balance sheet over € 20 million

- 2026 listed SME companies

- 2028 third-country companies operating in the EU with a turnover of more than 150 million €

Wide-ranging effects on the financing of companies and the commissions of designers

The sustainability directive affects the work of designers hired by the company, or companies that are part of the subcontracting chain. The directive and the related standards are of particular importance right now, if the design company operates in a subcontracting chain for larger companies or uses other companies’ products in its design work. With sustainability reporting, responsibility activities become visible and better compared. The level of responsibility will also affect to the received funding.

Thus, it is natural that companies want to invest by ordering services from subcontractors who comply with the standards as well as possible. Although reporting in accordance with the directive is facilitated during the transition period, according to OP’s large company review (2023), more than 40 percent of large companies have already changed their subcontractors or suppliers due to sustainability requirements.

Sustainability reporting can bring sustainability requirements to assignments and procurements; for example, those who work with interior architecture, industrial design, digital and service design, and strategic and business management design are most likely to receive sustainability requirements according to the directive. Sustainability reporting is a tool designed for the management level to make strategic changes to the company’s sustainability activities, and with that, it hopefully starts to be seen in the work of in-house designers and design teams as well.

In subcontracting, the ordering company may need detailed information about products or materials. Those who use other companies products in planning, such as interior architects, need information, for example, to evaluate the total emissions and carbon footprint of the space plan. The most affected will probably be the built environment, mining industry and textiles and clothing sectors, because of the long subcontracting chains and social responsibility issues.

Reporting therefore brings pressure to obtain information about the responsibility of the entire life cycle of products and materials. Responsibility information must be able to be given to the customer in a numeric format suitable for the report. EU is preparing a digital reporting base.

There is currently a lot of development work related to data processing, for example software and various emission counters. With the help of the calculator, the designer can analyse the most relevant emission sources, get information to support decisions and offer more sustainable options to the customer. However, there may still be challenges in the availability of emission data, so part of the calculation is based on estimates or averages.

The sustainability reporting standards cover the environment, social impacts, and governance perspective

Sustainability reporting broadly covers issues from the perspectives of the environment, social impacts and governance (ESG). These effects are reported based on special standards (ESRS, European Sustainability Reporting Standards).

The topics of the reporting standard used for the assessment are tabulated below. The standard has two parts: general information and instructions, and ESG topics. The subsections supplementing the topics at the heading level can be found in the standards. Industry-specific subsections are also forthcoming by EU.

Yleiset tiedot ESR1 ja ESR2

| Environment | Social | Governance |

| ESRS E1 Climate Change | ESRS S1 Own workforce | ESRS G1 Business conduct |

| ESRS E2 Pollution | ESRS S2 Workers in the valuechain | |

| ESRS E3 Water and marine resources | ESRS S3 Affected communities | |

| ESRS E4 Biodiversity and ecosystems | ESRS S4 Consumers and end users | |

| ESRS E5 Resource use and circular economy |

Designers should notice that reporting according to the standards is done as part of accounting, i.e. it becomes part of the operating report and financial statements of the ordering company. The company’s responsibility for sustainability information is similar to that for financial statement information.

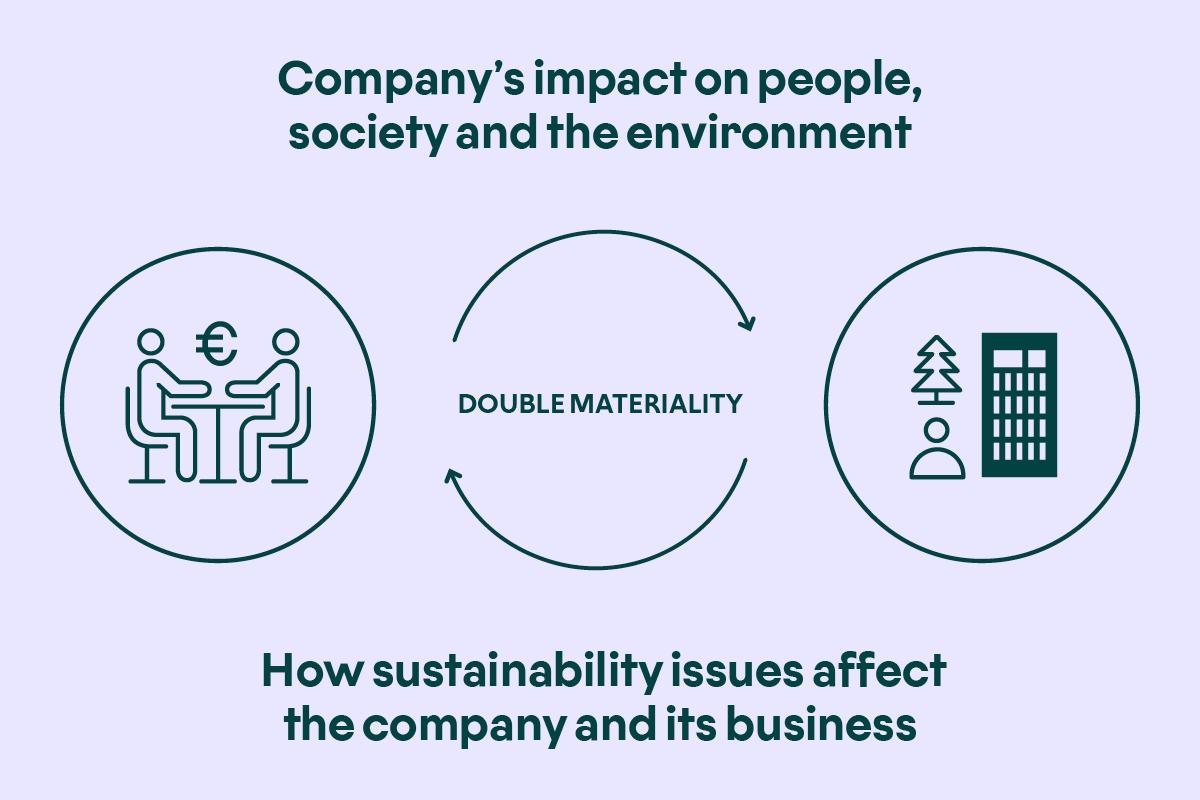

Double-materiality assessment takes into account the company’s effects on sustainability, as well as the requirements of sustainability for the company’s operations

With the help of the european sustainability reporting standard (ESRS), companies evaluate which effects, risks and opportunities are essential in its operations. The information must also include plans for the transition to a sustainable economy. All essential information in accordance with the standard must be given, and even those that are not essential are clarified with the help of information collected from the company’s operations. The auditor certifies the company’s sustainability reporting and gives a statement in his certification report on whether the sustainability report complies with the requirements for its preparation.

The report should be based on the perspective of double materiality. Double- materiality means the two-way nature of the assessment. The sustainability report must therefore include:

1) assessment of the company’s impact on people, society and the environment (from the inside out). Impacts include, for example, impacts related to the company’s own operations and the beginning and end of the value chain – also through its products, services and business relationships. A negative impact can be, for example, the use of child labor or the pollution of a river in the cultivation of cotton, in which case it is connected to the products of the design company in the textile sector through different levels of its downstream business relationships (e.g. seller – fabric processing – spinning – cotton farm).

2) assessment of how sustainability issues affect the company and its business (from outside to inside). This includes assessing material risks and opportunities in relation to the company’s development, financial position, financial performance, cash flows, availability of financing or cost of capital. For example, a water-dependent industry may identify the availability, quality and price of water as a business risk. Applying the directive to your own operations is worthwhile if you want to become a part of, or consider your own company as part of, the supply chain of a larger company.

Develop sustainability measures anyway

If the standards are not essential in your own business, the development of sustainability measures and related communication can be done more freely.

In this case, the company’s sustainability measures can be based, for example, on voluntary VSRS (Voluntary Sustainability Reporting Standards) standards or third-party certifications.

A small entreprise can start, for example, by clarifying their own values and which aspects of responsibility they can influence according to their own strengths. This increases the chance of real change and eases communicating it to customers, even if the enterprise doesn’t yet comply with standards or certifications. A small operator can get a competitive advantage from being agile.

However, the directive does not just mean reporting, but is one accelerating tool to bring about change. Responsibility is not a new thing for the design industry, and reporting will hopefully give designers the opportunity to do responsible design in line with their values. It is also advisable to communicate to customers that according to the principles of responsible design, the success of a product or service is not only measured in terms of revenue, but the evaluation should also take into account its positive effects on people and our planet. So it’s worth investing in good design, whether customer or company is reporting sustainability or not.

References

Author is a design researcher, who currently works as Ornamo’s sustainability expert. In her work, Tarja-Kaarina Laamanen helps designers in sustainability transition. She follows the legislation related to sustainability and addresses significange of the transition for the members.